OECD Global Outlook

The well-respected Organization for Economic Co-operation and Development (OECD) was founded in 1961 and is comprised of 37 member countries throughout the globe. Their “March 2021 Interim Outlook-The Need For Speed” lays out a positive assessment of current and future global economic activity.

First, Their Conclusions

The March OECD Outlook Changes from December:

- Projected 2021 global growth increased from 4.2% year-on-year to 5.6%.

- Projected 2022 global growth increased from 3.7% to 4% year-on-year.

- The OECD is projecting G20 2021 GDP growth of 6.2% year-on-year growth, up from 4.7%.

- G20 GDP growth outlook for 2022 rose from 3.7% to 4.1% [The G20 is a group of the 20 largest economies in the world.]

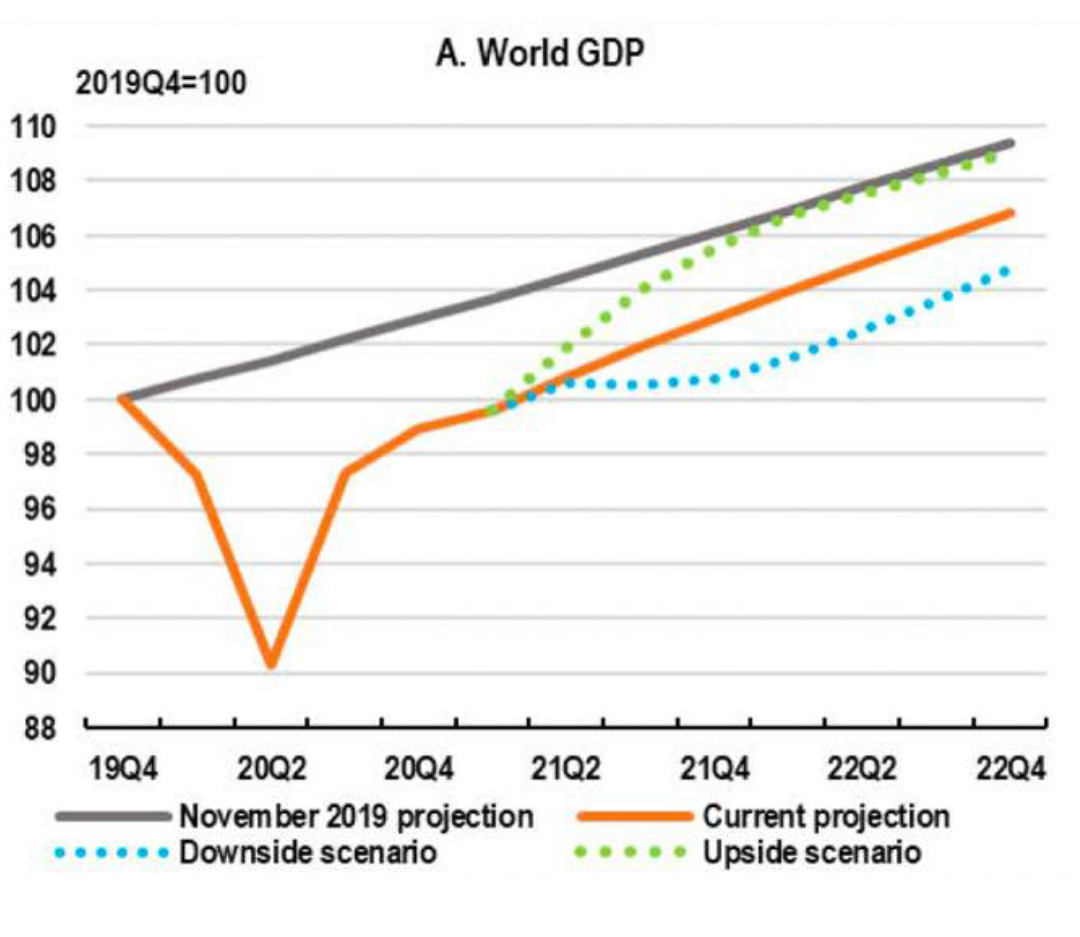

All in all, their current assessment of global economic activity is quite positive over the next 2 years. A key underlying theme is obviously the demand for goods and services that the population is eager to start buying again. The equally obvious theme is the need for global expansion of vaccinations to support the forecast as well as continued accommodative monetary stimulus, both of which are in their assumptions. The chart below shows OECD forecast changes since Q4 of 2019.

Rising Bond Yields/Inflation

The expectation of government stimulus paired with promising vaccination programs have fueled the economic rebound of the United States and treasury yields in 2021. Rising treasury yields on the surface tend to dim the outlook for equities and other risky investments giving the implications for rising inflation. On the flip side, higher yields and modest increases in inflation are indicative of improving economic activity and are what the Federal Reserve is actually encouraged by. So, it is a bit of a balancing act as to which way to think about it. It is understandable that the increase in the 10-year government bond yield from 0.31% a year ago to 1.66% today seems dramatic but keep in mind that the yield was 1.82% right before the pandemic began. Therefore, we are encouraged by the rapid pickup in economic activity getting overall interest rates back to normalized levels.

Once More on Shift to Value

I keep coming back to this movement in the market from a focus on large/mega cap growth to traditional value segments of the market. In other words, a shift from fully/over-valued growth stocks into “cheaper” stocks based on price-to-earnings and price-to-sales ratios among other measures. Our most recent change in portfolios continues to favor value over growth. Throughout both our Blackrock and Separately Managed Account (SMA) models, we have continued to rotate more capital toward value. In the upcoming month, we will rotate nearly 2% out of our international growth position and subsequently move 2% into international value positions. Additionally, we are continuing to add to our exposure in the Energy sector. With gas and oil prices on the rise, we believe the Energy sector is a good place to be going into the second quarter.

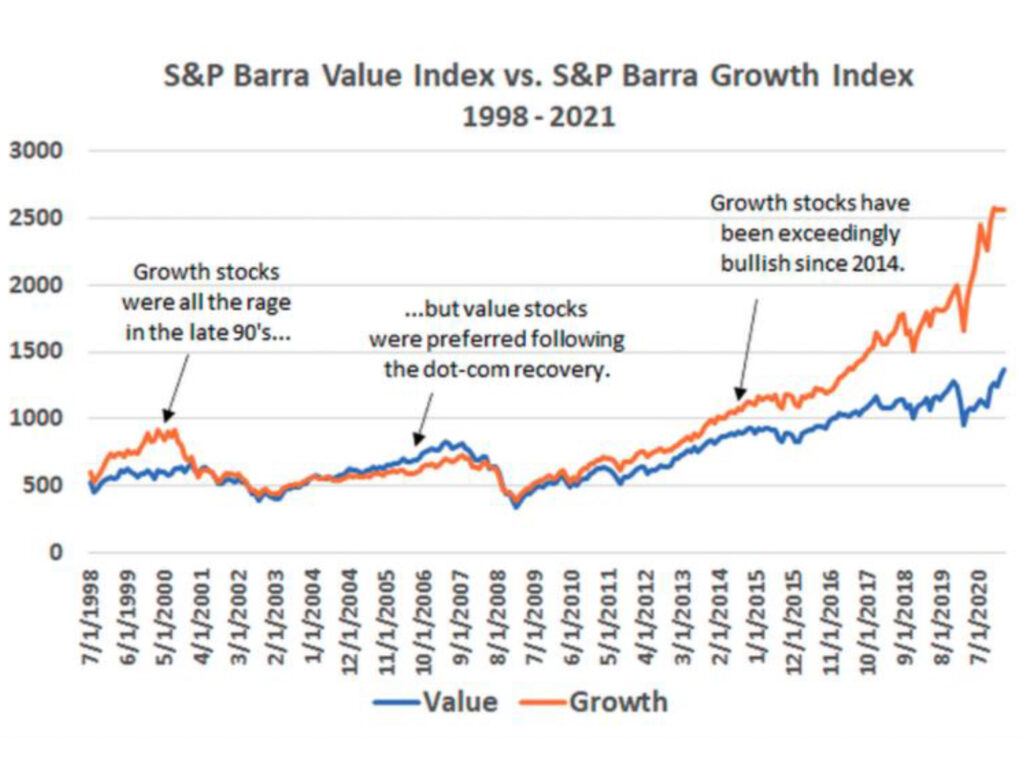

A recent article I read put it well saying that: “It’s admittedly tough to see, but what the market tends to reward changes over time.” The past several years has supported premium valuations for the very best growth stories, but at the expense of value stories. A sense of a renewed period of appreciation for value continues to build. Last month I showed you a performance chart of Buffett’s Berkshire Hathaway fund compared to S&P 500. Below is a chart with a similar message looking more broadly at an S&P index screened for value stocks and an S&P Index screened for growth stocks.

In addition, I have read about and agree that the value rally we continue to expect has more similarities between the current rebound and the one in 2000 after the dot-com bubble burst, than the recovery after the global financial crisis that tripped up value managers. There’s nothing structurally wrong with the economy now in terms of credit as there was after the financial crisis so I think the value rotation could last several years.

That’s a Wrap

March was a strong month and April is continuing the trend. Undoubtedly there will be periods of volatility in the coming months as the growth-to-value rotation continues. For now, it is nice to have things calm down a bit. As always, please reach out to any of us if you have any questions or needs.