For several years now, investors have been living in a world of historically low interest rates. For those in retirement or near retirement, that has not been the best world in terms of conservative income generation with which to live on. It also hasn’t been great for those who are contributing to regular savings accounts or are looking for low risk ways to generate a little income. Money market interest rates were stuck at around 0.01% to 0.03% not more than a year ago. Now they are yielding 2.25% or higher. Interest rates on government bonds have the same magnitude of increase over the same period with one-year Treasury Notes now yielding over 4.0%.

Higher rates also provide an incentive for people to save more. People are more inclined to spend their savings if they see that the returns on their savings are so low. I am over generalizing but you understand the gist of it.

Federal Funds Rate

Changes in the fed funds rate have a direct impact on the interest rates banks offer to customers for certificates of deposit, savings, mortgage rates and commercial lending rates, among other financial instruments. Raising the rate as the Federal Reserve (“Fed”) has been doing and will likely continue to do for the next several meetings is a tool to try and slow spending and thereby take some pressure off rising inflation. How long that will take and how high they raise rates is unknown but it may go on longer than people had originally hoped.

What is the Federal Funds Rate

In the United States, the federal funds rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight on an uncollateralized basis. Reserve balances are amounts held at the Federal Reserve to maintain depository institutions’ reserve requirements.

Institutions with surplus balances in their accounts lend those balances to institutions in need of larger balances. The federal funds rate is an important benchmark in financial markets.

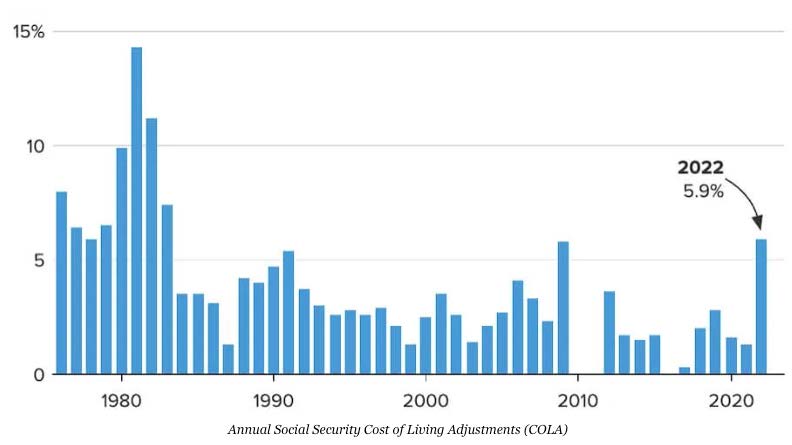

Increased Income/Social Security Cost of Living Adjustment (COLA)

As mentioned above, retirement planning is benefiting from higher interest rate environments given the substantial increase in interest income generation along with asset preservation. Higher rates also help consumer savings as inflation increases. As inflation rates rise, our goal is to invest fixed income assets at increasingly higher rates to keep pace with inflation.

For 2023, Social Security beneficiaries will enjoy an estimated increase in their benefits on the order of 10%. If so, that would be the third highest increase since COLAs began in 1975. The highest and second-highest COLAs were 14.3% in 1980 and 11.2% in 1981. By law, there will never be a negative COLA applied to future benefits. The actual increase will be announced in October. If we do get a 10% COLA increase for 2023, it would boost the average Social Security retirement benefit by about $150 a month in 2023. The 5.9% COLA for 2022 brought the retirement benefit up by $92 per month whereas, in 2021, the average increase of a 1.3% COLA was $20 a month.

Good News for Homebuyers

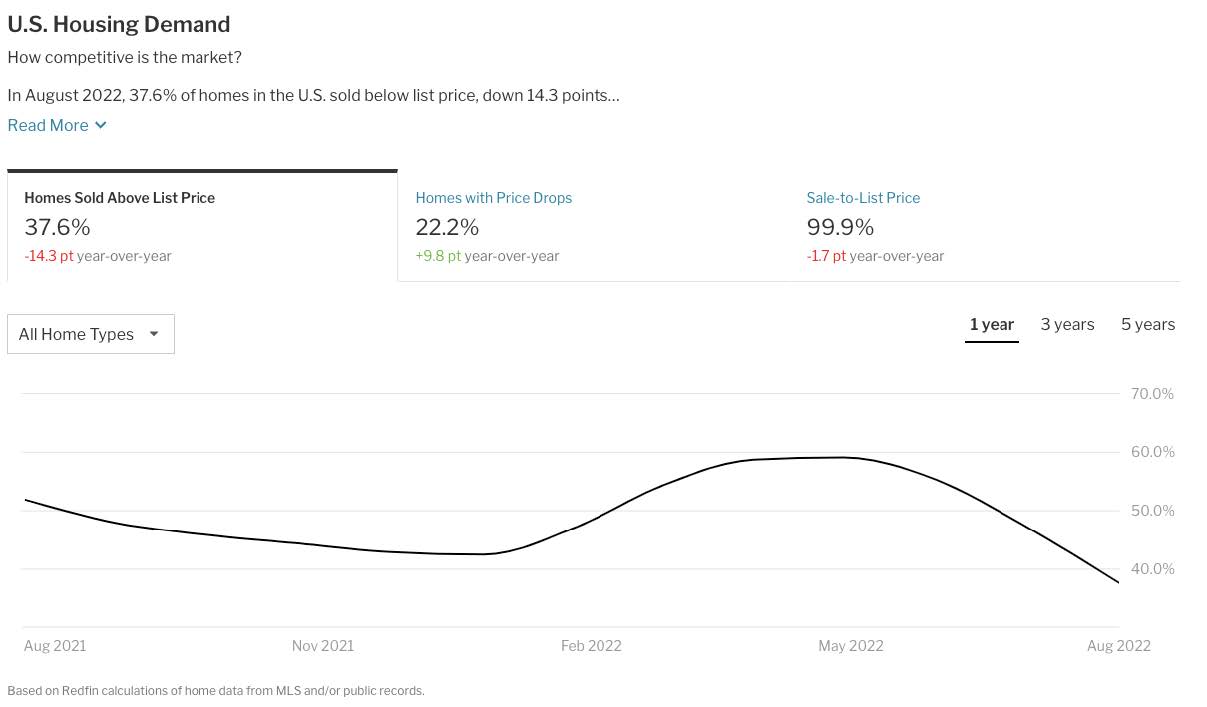

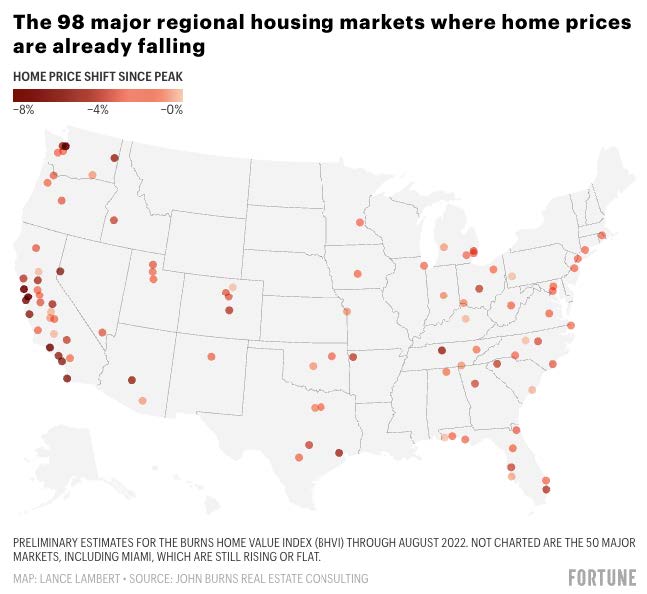

Mortgage costs have risen rapidly in the past 6 months which everyone knows. In that same timeframe, we have seen the housing market slow and price reductions pick up. The days of people rushing to buy whatever home comes along for fear of even higher prices in the future are diminishing or have simply gone away. The length of time that homes are on the market has increased to 30 days or more in hot markets around the country. So, for buyers who simply got tired or gave up chasing a new home, the outlook is improving. It has become a “buyers’” market out there and “sellers” know it. For prospective home buyers, price reductions and rising mortgage rates can balance out leaving them in a similar financial situation as they were before. In addition, lower valued homes come with lower property taxes and lower home insurance rates which also improves affordability.

Pending home sales this past July vs July 2021 declined over 22% nationwide. The largest decline was in the West at over 31%. Just in the past few days, Opendoor Technologies, a pioneer of a data-driven spin on home-flipping known as “iBuying”, announced it lost 42% on all its August resales. I wouldn’t think individual homebuyers out there who have been squeezed out of the market by such companies are crying for them.

All signs point to these trends continuing. Our advice to those who are still looking or are considering getting back in the market for a new home is to sit back and let the inventory of homes for sale grow in your targeted geographies. There is no longer a need to make offers that waive inspections or other important contingencies that buyers have been making just to get to the front of the line. Time is on your side.

Wrapping Up

It goes without saying that there are more moving variables impacting all parts of our domestic and foreign economies than we have experienced in a long time. The potential for the housing market to contract on the order of what happened during the financial crisis of 2009 is remote in my view. There are many statistics I could reference but key is that consumer balance sheets are in much better shape and the financial system is in much better condition than it was back then.

Short-term interest rates will continue to rise as Fed Chairman Powell has indicated. We are beginning to see small month over month decreases in the Consumer Price Index but focus is always on year-over-year numbers which ticked up very slightly in the August report. That is the headline number that everyone is watching.

We will continue to pursue income strategies that keep pace with rising short-term rates. The equity markets are digesting interest rate changes in a choppy, volatile fashion that we expect to continue for the foreseeable future. We have been through similar types of environments before and feel strongly that maintaining conservative, value oriented portfolios is the right strategy.

As always, please reach to me or anyone on the team if you have any questions or would simply like to have a more in-depth conversation on the state on the markets.