For anyone that has traveled by air in the past 12-18 months, you have experienced firsthand just how fast demand for air travel has grown. Even with significant increases in air fares and a looming recession, more and more consumers continue to get back into travel mode. How long this rising demand continues is anyone’s guess but, in an attempt to put some data and forecasts together, I will give it a try.

Prioritizing Travel Experiences Over Buying Stuff

Believe it or not, a study has actually been done to determine what “sparks people’s in-the- moment happiness”. (“Spending on Doing Promotes More Moment-to-Moment Happiness than Spending on Having” University of Texas at Austin, May 2020). The results: Happiness was higher for participants who consumed experiential purchases versus material ones in every category, regardless of the cost of the item. Going to sporting events, dining out, traveling away from home for pleasure or other experiences beat out buying things like jewelry (who knew), clothes or furniture. I wouldn’t think the conclusion here would surprise many people but it is a trend that is contributing to the surge in demand for travel experiences.

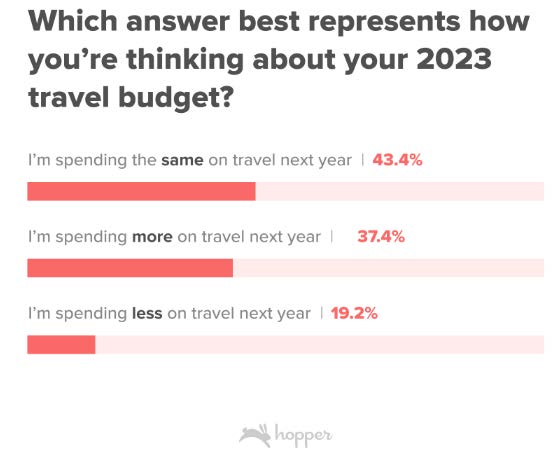

Consumers, notably high-income ones, are able to satisfy their urge to travel because, even though hardly a day goes by without talk of recession, labor markets remain very tight, wage growth continues and savings have held up in the face of sharply higher inflation. Below is a survey done by travel firm Hopper on travel plans for 2023. Eighty-one percent of people are planning to spend the same or more on travel in 2023. Note that Hopper users are predominately Gen Z and millennial travelers.

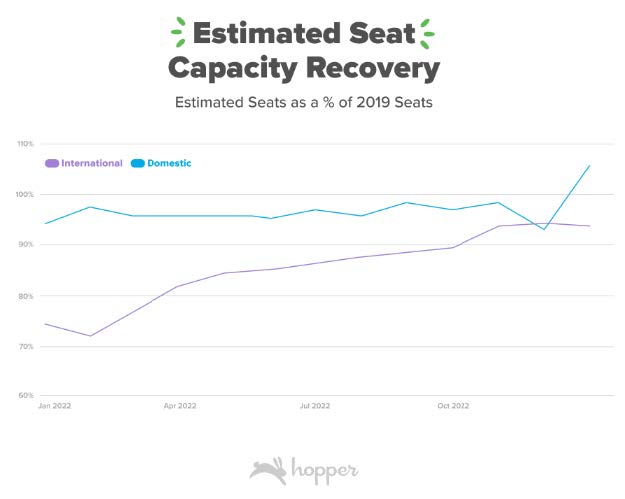

To meet this demand, airlines have been swapping out smaller planes for larger jets to capture rising demand with fewer flights. These equipment swaps have allowed airlines to bring back much of 2019 seat capacity, while keeping flight volume below 2019 levels. Below is Hopper’s estimation of seat capacity recovery. They note that given the Boeing 737-Max 8 situation and pandemic supply chain issues, many airlines are waiting for new aircraft deliveries. More on plane deliveries below.

Leisure Booking Numbers

The chart below shows that through the end of March 2023 leisure travel bookings were up 31% from March of 2019. Leisure travel bookings were up 25% year-over-year-to-date growth between 2022 and 2023 which is impressive.

While it is certainly hard to confidently say leisure bookings will remain in an upward trajectory, the opening up on the Greater China region, which has been slow to date, could provide significant upside to growth in future quarters. Through the first quarter of this year, the strong recovery in China’s domestic and international markets helped China increase passenger traffic to be within 15% of 2019 levels for the same period. Predictions are that China, and the Asia Pacific region in general will continue to recover to pre-pandemic levels providing strong global growth even as other global regions possibly slowdown.

Commercial Travel Booking Numbers

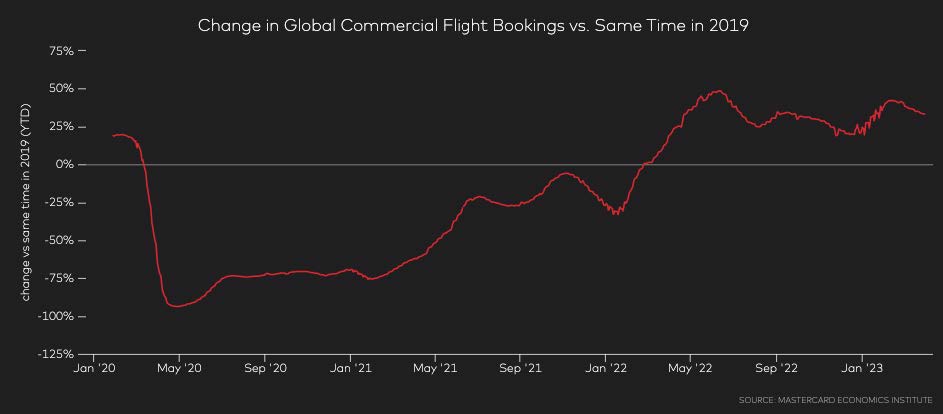

Global commercial flight bookings began recovering at a slower pace than leisure but have since caught up as the chart below represents. There do exist some risks to commercial booking trends as companies look to control costs in the current, rather uncertain, environment. That said, it seems that demand for in-person meetings remains strong with bookings well above pre-pandemic levels measured back to the same period in March 2019.

Takeaways From the International Air Transport Association (IATA) Q1 2023 Chartbook

IATA measures travel trends in “revenue passenger-kilometers” (RPKs) which more accurately reflects travel recovery trends in financial terms, rather than being measured in terms of bookings as above.

Passenger Traffic

- Recovery in global air travel demand seen throughout 2022 continued into Q1 2023 climbing to only 12% below pre-pandemic levels.

- Industry wide RPKs rebounded to 85.9% of Q1 2019, up from 68.5%for the full year 2022.

- International traffic routes between Europe and North America are actually 4.5% above pre-pandemic levels and Europe-Central America only 2% below.

- Pent up demand due to the reopening of China has led to a surge in all routes between Asia Pacific and the rest of the world and is expected to continue to drive traffic recovery throughout 2023.

- Premium RPKs have been recovering faster than economy RPKs even in the face consumer uncertainty.

- Available seat capacity, measured in “available seat-kilometers” (ASKs) has risen in line with demand for air traffic.

- Passenger load factors (% of available seat kilometers) are close to 2019 levels for all regions demonstrating strong demand for air travel worldwide.

Looking Ahead

- Worldwide passenger traffic is expected to fully recover to 2019 levels by 2024, buoyed by developments in China and the Asia Pacific region.

- North America as well Latin America & the Caribbean traffic expectations are for a full recovery this year.

Aircraft Deliveries

- North America region, primarily in the US, will account for approximately one-third of global aircraft deliveries for 2023.

- Deliveries in 2022 were already above 2019 levels and are expected to grow by an additional 72 units this year.

- Planned deliveries for 2023 support the region’s expected full recovery of passenger traffic this year.

- Deliveries are expected to be primarily narrowbody jets.

- Asia Pacific region will account for the second-highest volume of aircraft deliveries in 2023 (29%), a 21% year-over-year increase off a low base and accounts for the largest share of widebody orders.

- The slower recovery in traffic for the region contributed to delayed deliveries.

- Europe region will account for the third highest volume of aircraft deliveries in 2023 (26%) and the second largest share of widebodies scheduled for delivery in 2023.

- Widebody deliveries are up 20% year-over-year but remain below their pre-pandemic levels.

Wrapping Up

In the face of headwinds such as sharply higher inflation, declining consumer confidence, higher interest rates and general economic uncertainty as the year unfolds, demand for air travel is expected to continue to grow reaching or exceeding pre-pandemic levels by the end of 2023.

This Memorial Day saw air travel surpass pre-pandemic levels even though the average domestic roundtrip cost is 4% higher than in 2019.

Baring the unpredictability of global economic activity, I believe the demand for travel experiences will continue to grow well into 2024. Inflation is expected to continue declining, albeit slowly, into next year. And just this past April, wage growth exceeded the rate of inflation by over 1%. Anecdotally, it seems that the more people enjoy the “stay-at-home” work opportunities, the more they want to travel.